CONSUMER SURVEYS FROM Deloitte and others consistently report strong intentions by households to purchase more of their grocery and packaged goods online. This has been true for many years. I suspect there’s some response bias in play.

A recent Retailwire.com discussion raised this issue in the context of a gap between measured shopper interest in online CPG purchases and the less-than-dynamic efforts by most CPG companies to take full advantage of the opportunity. Are they missing the boat? Or are they just taking a prudent approach in the face of greater complexity?

Here’s my take:

Until the perspective shifts from, “How will we sell our products online?” to “How will we help households better manage their pantries?”, I believe this business will continue to be “just around the corner” for CPG, as it was in 1997.

Certainly, splintering the grocery shop into dozens of weekly decisions, transactions and deliveries is no way to help shoppers streamline their consumption routines. This was then and remains now the fallacy of the “consumer direct” concept. Disintermediation is bunk.

A re-consideration of the grocery basket and how it arrives to the home is another story. That requires a solution orientation on the part of the service provider (the retailer). Never-run-out tools, bulk shipments of high-consumption items, and secure unattended delivery have all been well-received in the past. Rapid delivery mechanisms from Amazon.com and others may add traction in areas with urban density, but the relevance will vary widely by location and purchase occasion.

Unfortunately for brands, these emerging concepts will not simplify the in-store shopper marketing imperative in any way. They do add, however, a whole new set of required practices for brand promotion and interfacing with online channels and shopper marketing outside the store. Set against the hard reality of somewhat inelastic total demand, that’s a very tough formula.

RIGHT NOW CONTENT MARKETING is the name of the game. That’s Content with a capital C, which is presently a thriving business in the ad agency domain. The idea is to influence the trends that flow through social and mobile media by inserting Content on behalf of brands.

There are many ways to accomplish this — ranging from hiring ringers to post favorable reviews and spam blog comments, to sharing genuinely valuable consumer information like product usage tips or recipes. It is also desirable to monitor Content posted by others, then respond as needed to amplify, rebut, or influence perceptions.

The motivation is, I think, largely fear-based. The social-mobile frenzy generates tons of uncontrolled consumer sharing, both pro and con, accurate and inaccurate. No doubt there are also dirty tricks being played every day by competitors bent on undermining their rivals. Brands lose sleep over losing control of their messages and so they hire hip young firms to help them create and spread content of their own.

The trick to making Content work is to put enough of it in front of the folks the brand wants to influence, especially the ones capable of influencing others — like bloggers and social media divas. The agencies are supposed to ensure that the Content is both artful and discoverable by the target audience. Hipness and coolness are good traits too.

So the goal is to create the right Content and embed it within the right Context, in order to better drive Commerce. A key attribute to making all of this work is authenticity — the perception that the Content is believable, relevant, and true (probably in that order). The new Content Marketing agencies are all over this, of course.

Today I shared a bit of content of my own on RetailWire.com as part of a discussion, Which Came First? The Content Or The Egg? It make me think about the quip about sincerity most often attributed to Groucho Marx, who is pictured here in the classic film, “Duck Soup.” (It may actually have been first uttered by French dramatist Jean Giradoux, but Groucho is funnier.)

Here’s my take:

It seems “content” is a wheel that keeps on rolling. Remember the “content is king” slogan that was popular at the peak of the dot-com frenzy? Its relevance then was the hunger for product data and other information needed to populate the new web sites. If you build it, you have to fill it with something, right?

Content was soon displaced by “commerce” as folks got the shopping cart and delivery mechanisms worked out and consumers got used to the idea of shopping remotely. After a period of more or less centralized control, the social-mobile reality has caused user-created content to explode, but in an entirely uncontrolled manner.

It is into this chaotic environment that the new content marketers are venturing. They hope their organized campaigns will somehow float above the SoMoLoMe din, resulting in a degree of influence over brand perceptions. A whole industry of B2C content marketing agencies is emerging to service this trend.

The risk is that these messages drown in a vast content sea in which the relevant mixes with the contrived. I don’t believe brands will win in this environment simply by opening the floodgates or turning up the volume.

Only quality and authenticity can win in such a content-flooded environment. To paraphrase the sage, Groucho: If you can fake that, you’ve got it made.

ONE OF THE SIDE EFFECTS of the “showrooming” panic which seems to grip some of America’s big box retailers has been a flood of learned and not-so-learned opinions from learned and not-so-learned analysts and observers.

Showrooming anxiety emerged during the 2011 holiday selling season, when chains like Target and Best Buy were revealed as victims. Shoppers were inspecting and comparing merchandise in their stores, then using mobile apps to find and order the desired items at lower prices from places like Amazon.com and Buy.com. The story had a second surge in media coverage during April, when Best Buy reported soft sales and the departure of its CEO Brian Dunn. There are too many articles to count about this. How important is it, really?

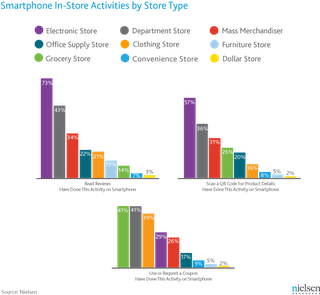

The Pew Internet & American Life Project reported Jan. 30 that about one fourth of shoppers had used a smart phone at least once to check a price in a store during the last holiday period. The release did not specify which types of products were checked most. I’d bet a month of sales that the skew was heavily toward high-consideration purchases like TVs and major appliances.

Nielsen recently released findings that suggest there is indeed a significant variation in impact of mobile device use across retail channels. Nearly three fourths of respondents said they used a smartphone to check prices on a consumer electronic item, while more than half said they had scanned a code with their phone in a CE store. This behavior was much less prevalent in most other product categories – but not zero.

The New Transparency Clearly there is much more we need to understand about this shopper behavior complex — not only about how shoppers are altering their habits around certain purchases, but also regarding what brands and retailers should do about it.

To that end, DemandTec, an IBM Company, is now sponsoring a RetailWire survey with specific focus on how retail practitioners think brick ‘n mortar retailers should combat showrooming.This is a worthy undertaking with potential to help surface superior thinking about the new era of price transparency:

We’ll interpret findings from this study here later this summer.

Absent investigations like these, showrooming may remain a buzzword excuse used by unimaginative retailers to explain away their mediocre performance in the face of increasing price transparency. It’s already a hot-button headline word for the herd of analysts and reporters who interpret consumer behavior based on instinct rather then empirical analysis.

I’m concerned that retailers who focus too narrowly on defeating showrooming are at risk of actually defeating their own shoppers. I propose an alternative: Focus on helping them get the best deal possible — from your bricks or clicks.

It could be that showrooming is not all bad, if we pay systematic attention. It could be just the reality check you need on your price image that could enable early corrective action.

Retailers collect slotting, display, and promotional allowances from manufacturers in exchange for putting products on their shelves. In some sectors, the net profits from these activities exceed the net profits from sale of goods. A lost sale, while unfortunate, is not a fatal occurrence. And manufacturers may still have powerful incentives to pay allowances to physical retailers who put their products on display — even if some resulting purchases take place online.

ALL THE RECENT chatter about “social media for business” is driving me around the bend.

For some time now, I’ve been searching for a terminology that would rescue us from imprecision and allow a meaningful business conversation to take place around the impact of smart phones within the retail environment.

At the National Retail Federation Conference and Expo two weeks ago in New York, the presentations and pitches frequently turned to the impact of social and mobile media, and I kept cringing every time I heard it. Here’s why it bugs me so much:

When new business phenomena have arisen in retail marketing, sloppy terminology frequently led to poor initial understanding of the business opportunity. Often it is due to a choice of words laden with confusing prior connotation – or the absence of a suitable term.

We sometimes used “consumer” and “shopper” interchangeably; now we distinguish between those two customer roles. We spoke of “manufacturers” or “vendors” before the term “brand marketer” was introduced in the mid-90s.A deficient thought vocabulary renders some concepts virtually unthinkable.

In Your Facebook

Today, most of the marketers and solution vendors obsessed with “social media” are in fact formulating new ways of delivering one-on-one messages to targeted shoppers and attempting to influence what they do and say on social networking sites. It’s undeniable that one particular application – Facebook – happens to be used heavily for social play and sharing of consumer lore. Marketers are dazzled by the massive “audience” it has accumulated and are salivating to exploit the opportunity. How fortunate for Facebook investors.

But setting up corporate pages on Facebook or Twitter does not a strategy make. Indeed the existence of these pages implies a broadcast mentality – from us to them. Despite the open visibility of customer comments on the wall, there seems to be relatively little interaction between consumers on these pages. Old comments get quickly buried behind newer ones, and only our social media hired guns bother to track and analyze them – in reports calculated to justify their existence.

Regardless of the channel, shopping is primarily about each individual’s personal success – get the best deals; satisfy my needs most efficiently; manage my budget; impress my friends; etc. When a shopper turns to his or her personal mobile device to access tools to enhance in-store success, it’s a very personal action motivated by very understandable self-interest.

Getting Personal

I submit that when it comes to tapping shoppers via those pocket two-way radiowave computers we call smartphones, there’s very little “social” about it. It’s not social – it’s personal.

If we conceive of the mobile device as a personalized channel for interaction between retailers or brands with individual shoppers or consumers, then we would do well to set aside the imprecise term “social media” and start talking shop. These new media are personal media. Much of what happens on them may be social in nature, but everything that happens on them is personal.

The personal mobile device is taking shape as a personal nexus, where online, in-store, social, and commercial communications converge in unique combinations tailored by and for each individual. Each of us shifts roles at will, according to our objectives of the moment – searcher, receiver, reporter, sender, aggregator, re-transmitter, gatekeeper, purchaser, advisor.

Businesses that hope to play effectively in this incredibly fluid and fast-changing media environment had best get their minds around the personal nature of the shopper experience using mobile devices. When we discuss our strategy for personal media, the marketing mindset shifts in what I think is a constructive direction. Better decisions and practices must surely follow.

As for me, I have nothing against online friendships; but when it comes to business you may count me as anti-social. My reasons? Well, they’re personal.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager

CONSUMER SURVEYS FROM Deloitte and others consistently report strong intentions by households to purchase more of their grocery and packaged goods online. This has been true for many years. I suspect there’s some response bias in play.

CONSUMER SURVEYS FROM Deloitte and others consistently report strong intentions by households to purchase more of their grocery and packaged goods online. This has been true for many years. I suspect there’s some response bias in play.