I CALL IT the Paradox of Scale: Grocery chains keep getting bigger, but industry profit performance remains stagnant.

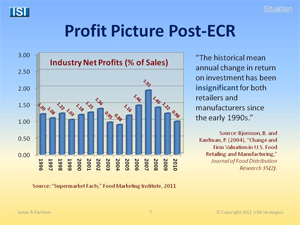

It’s been a doggedly persistent trend. Between 1992 and 2009, the top 20 U.S. grocery retailers increased their cumulative market share from 39% to 64%, according to the U.S. Economic Research Service. Meanwhile from 1996 to 2010, industry net profits have hovered consistently around 1% of sales, according to the Food Marketing Institute.

These facts seem to run counter to intuition. After all, bigger chains are supposed to have top-of-the-line executive talent, fine-tuned supply chains, advanced IT systems, greater buying clout and economies of scale. A deeper look reveals the paradox: Bigger chains also suffer from intensified store operational complexity, larger assortments and poorer visibility from the home office.

Bottom line – as chains expand, store performance management gets much, much harder. This begins to explain why out-of-stocks continue to run at 8.2%, unchanged in 15 years, yet 78% of items sell fewer than 3 units per week. It begins to explain why as many as half of all authorized in-store display promotions are never erected or erected late. It begins to explain why most retailers have no effective process in place to ensure or even monitor everyday planogram compliance.

Where some may find darkness and frustration in these statistics, others identify a golden opportunity. The In-Store Implementation Sharegroup identified tens of billions of dollars at stake – a rich prize indeed. Bold retailers and marketers who commit to improve retail compliance practices in the next few years should gain a distinct performance advantage over their less nimble competitors.

In-Store Implementation is not an isolated solution; it’s a multi-threaded initiative that incorporates improved in-store sensing and measurement; better inputs into planning processes; a performance-oriented culture; and alignment of trading partner resources. Many of the enabling practices and tools already exist, ad hoc. Still needed is an organizing principle that can tie them together into an effective set of best practices for the industry.

In just two weeks, a select group of industry thought leaders will come together to explore how to make this ambitious agenda a beneficial reality. They will be participating in a pre-conference workshop at the LEAD Marketing Conference in Rosemont, IL, on Sept. 19.

The workshop is presented by the In-Store Implementation Network, a membership organization with an educational mission centered on advancing awareness and knowledge of ISI practices. The group boasts more than 1,400 practitioner members in 28 countries who share a common goal – the establishment of a culture of performance at retail that makes stores work better, shoppers more successful and businesses more profitable.

Thanks to the generous sponsorship support of our friends at Gladson, ISI Network has assembled an all-star faculty to address key facets of the opportunity. The workshop format is intended to ensure that participants will leave the half-day event with a fresh perspective and practical ideas that may be applied immediately to their own ISI business challenges. As Executive Director of the ISI Network, I will be the lead facilitator of this workshop.

A few seats remain available; admission is complimentary to retail and CPG practitioners. I look forward to greeting many of you in Rosemont!

To register for the LEAD Marketing Conference, click here.

For a detailed agenda about the ISI Pre-Conference Workshop, click here.